What if we invented the pension again from scratch?

Answer: Wellbeing and resilience - not just a paycheque.

It's that time of year again - I'm back in one of my favourite places in the world. The Dolomites. The usual wintery photo attached.😎

A year since I last hit the ski slopes, and as always, the first few runs are a humbling exercise in muscle memory! This time, the penny dropped: it's all about whether you have flat or tilted skis. Such a simple principle. If I were learning from scratch today, surely that's where I'd start.

Big vistas inspire big thinking. A recent report from the Arketa Institute gave me a lot of food for thought on the flight out, and planted the seed for this article's central question.

Imagine that no pension system exists yet. You've been asked to design one from scratch.

Your brief: help people live with dignity and security in later life, in the context of the world as it actually is today.

Would your design start with what we have now?

I don't think you would. And I think exploring why tells us something important -not just about the system, but about what we can do differently, starting today.

This article is a longer one. It's not an easy question to answer quickly! - so grab yourself a cup of tea, or save it for a quiet moment on your commute.

A potted history: the pension was never meant to be this

Did you know the first modern pension was essentially a bonus for living longer than expected?

When Bismarck introduced Germany's state pension in 1889, the retirement age was set at 70. Average life expectancy at the time was less than 45.¹ The pension wasn't really a financial product - it was a rare pay out for an unlikely outcome.

For most of the 20th century, pensions evolved into something more meaningful: a guaranteed income in later life (and still does in the UK public sector). The "defined benefit" era. You worked, the organisation promised you a stable income, and the risk sat with the employer.

Then came the shift. "Defined contribution" pensions - the type most of us have today - moved the risk squarely onto you. Instead of a promised income, you get a pot of money invested in global financial markets, with the hope - though nothing in the way of guarantee - that it will be enough.

Today, pension assets represent roughly a third of all global financial assets. That's an extraordinary concentration of economic power. And with that power comes enormous inertia. Pensions have become one of the primary engines of what economists call the "financialisation" of the economy - the growing dominance of financial markets over how we organise and value everything from housing to healthcare to energy.

The tragedy of horizons

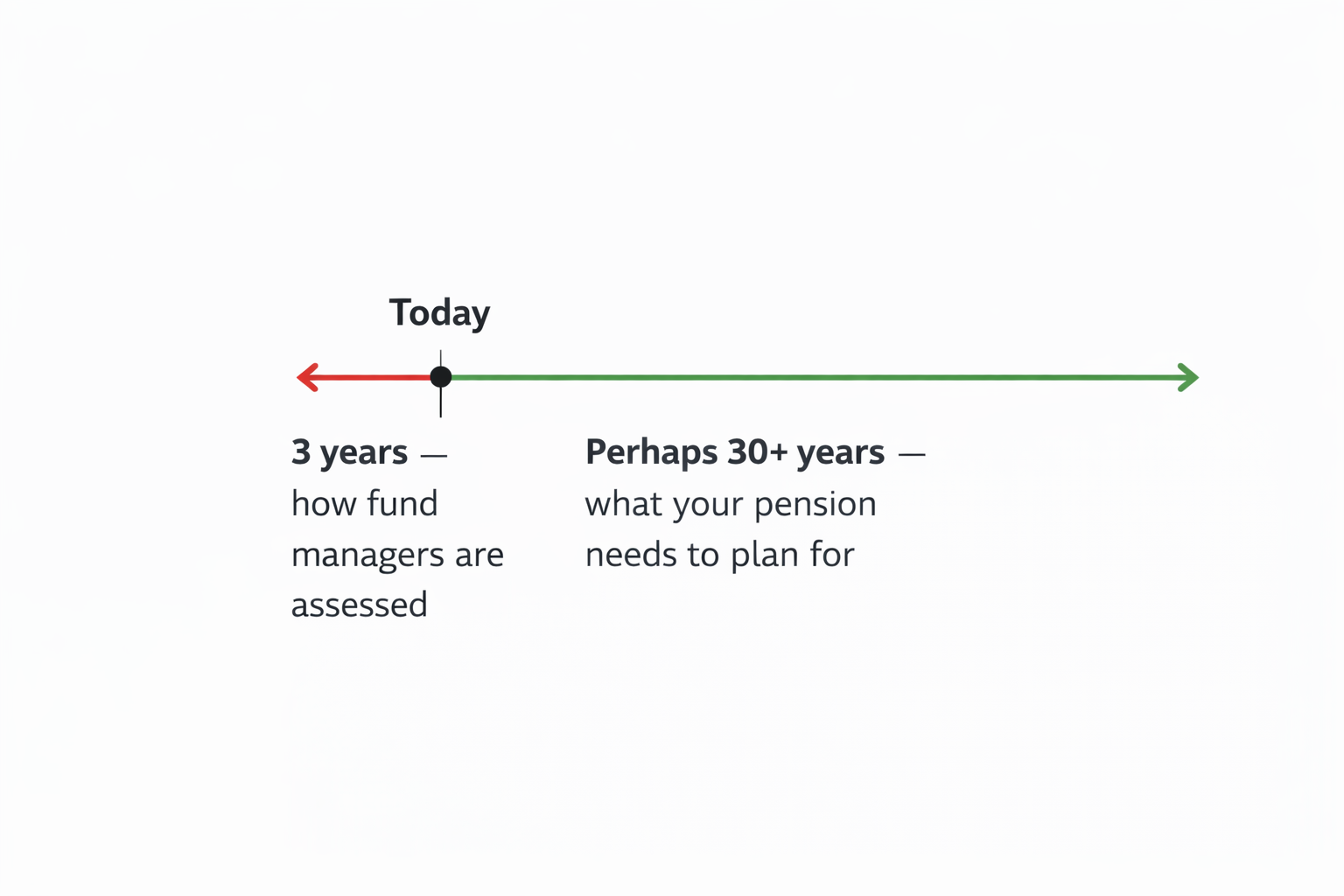

Mark Carney, when he was Governor of the Bank of England, coined a phrase I keep coming back to: the Tragedy of Horizons.

The idea is this: the financial system is structurally incapable of dealing with risks that play out over long timeframes. Because what gets measured - and therefore managed - is performance over the past three years. Not the next thirty or more.

Think about that for a moment. Your pension fund manager has a legal duty to act in your best interest - but in practice, that obligation tends to get interpreted through the lens of recent performance. The metrics that drive their decisions are backward-looking. Yet the whole point of a pension is to provide for a future that is decades away.

Is past performance over three years really a good indicator of what markets will look like in 2060? I'd suggest not - especially given what we know is coming.

A different world

When pensions were first invented, annual global carbon emissions were a fraction of what they are today. We hadn't crossed a single planetary boundary. The idea that human civilisation might face existential risks from its own economic activity was not a serious mainstream conversation.

Today, six of our nine planetary boundaries have been breached.³ Climate scientists openly discuss scenarios involving the collapse of civilisation. We have watched a month's rainfall fall in a single day in parts of Germany. We have watched entire communities burned to ash in Canada.

And climate is not the only threat on the horizon. The risk of nuclear armageddon, engineered pandemics, and AI deployed by malevolent actors are all part of the same picture - a world in which the assumptions of stability that underpin our financial system are increasingly hard to take for granted.

If we were designing a retirement system today, knowing all of this, would we really build one that pumps the majority of our collective savings into financial markets - markets that are both exposed to these systemic risks and, in many cases, part of the root cause of them?

Our conundrum

We've all grown up with a belief that markets recover. In finance, we call it "mean reversion". Markets go down, but they come back up. History says so. Recent history gives us the expectation they do so quickly.

That logic holds - until it doesn't. And here lies the conundrum: believing it won't hold is genuinely, psychologically difficult. It requires accepting something that feels almost unthinkable - until it happens.

Take the 2021 floods in Germany's Ahr Valley. In a single night, a region that had no serious flood warning, no evacuation plan, and no expectation of disaster lost 190 people and €33 billion in damage.² It was the deadliest flood in Germany in living memory - and 75% of the deaths occurred outside the official flood hazard zones. People simply couldn't believe it was coming. Until it was.

That is the nature of a true black swan. Plausible in theory. Unbelievable in practice - right up until the moment it isn't.

For financial markets, the equivalent risk may not be a single catastrophic event. It may be something subtler: the gradual - or sudden - erosion of the optimism that underpins financial valuations. Markets don't just price assets; they price belief in the future of the system. If that belief falters, and takes a long time to return, the logic of "markets always recover" breaks down in exactly the way that matters most - during the decades when you're supposed to be drawing down your retirement savings.

I'm not saying abandon your pension tomorrow. But I am saying: financial markets are becoming too risky to rely on completely.

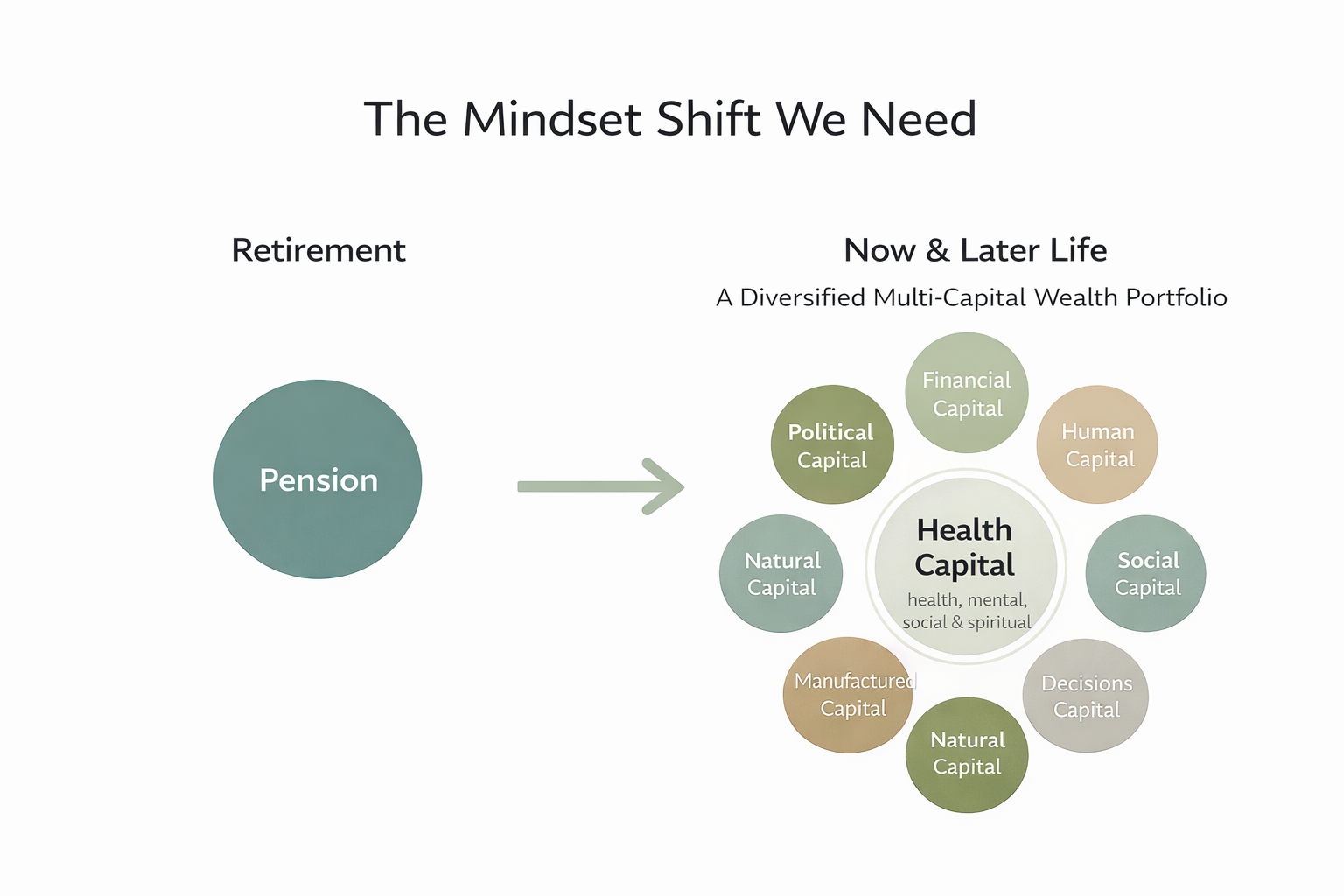

So what would we design instead?

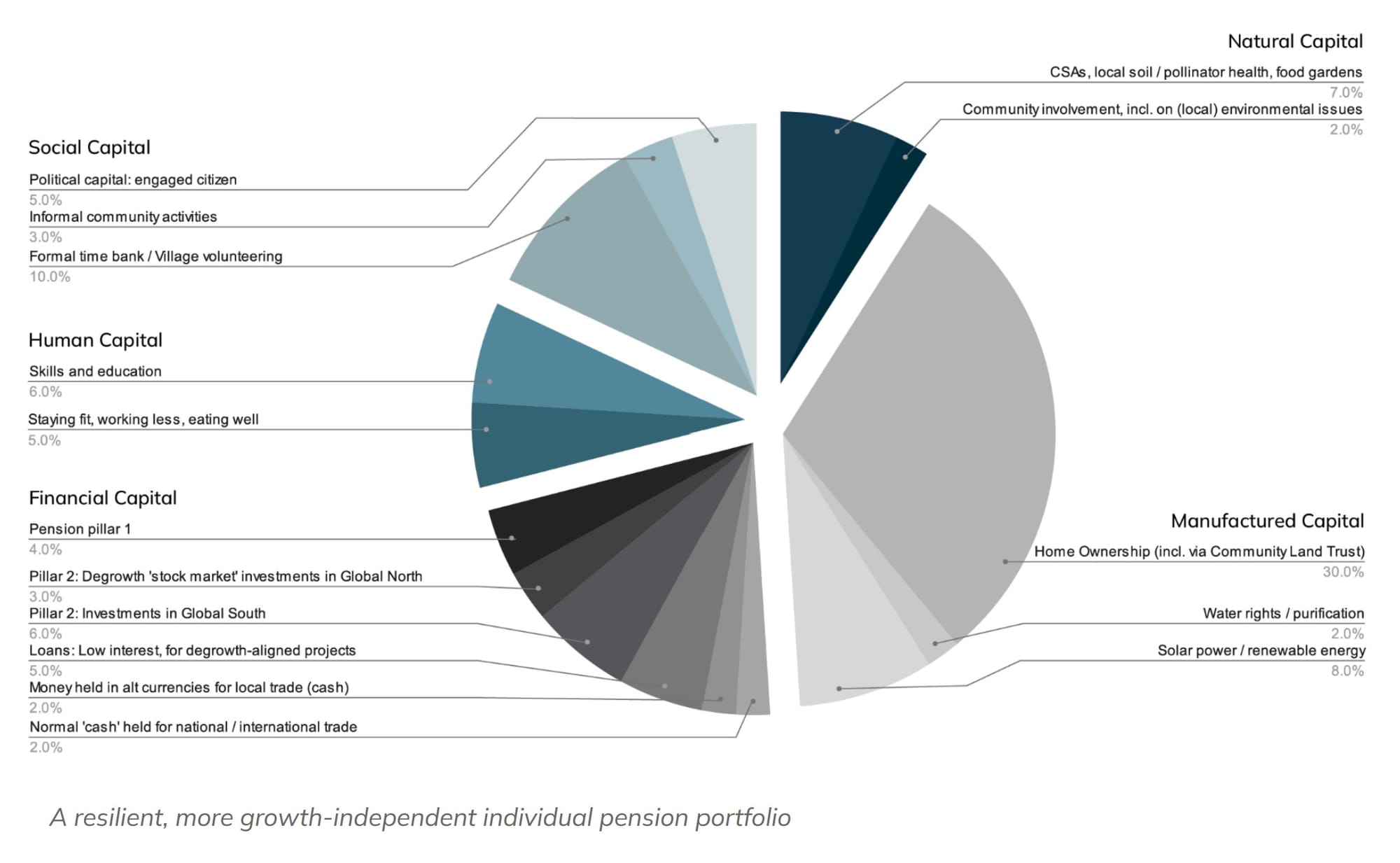

The Arketa Institute for Post-Growth Finance - a non-profit research organisation working to align the financial system with ecological and wellbeing needs - has proposed something they call a multi-capital approach to saving for retirement. Instead of planning for a future pay-cheque, you plan for future wellbeing.

Their stylised alternative retirement portfolio (pictured below) is telling. Financial capital accounts for only around 22% of your whole wealth (compared to 51% without). A few things follow from this:

- Less of your wealth feeds financial markets that often fund extractive growth

- The financial capital that remains is directed purposefully - towards degrowth-aligned investments rather than default index funds propping up the old economy

- The traditional pension logic relied on compound financial growth to fund later life benefits cheaply over decades - that engine is now more uncertain

- The shift from defined benefit to defined contribution was partly a way for employers to move financial market exposure onto you. What if instead (assuming could be favourable), employers committed to funding certain benefits in retirement directly rather than routing everything through financial markets?

Good news too. We can start to implement a multi-capital approach in a self-directed way, right now. And if more of us do, it becomes inspiration for something bigger - systems change from the ground up.

Here's how I think about the different capitals, and what each might mean for you.

🏃 Health capital - probably your most important asset

Just as money invested early compounds over time, so does health. The habits you build now - across all four dimensions of physical, mental, social and spiritual wellbeing - compound quietly over decades.

You might religiously put money into your ISA each month. But are you taking your long-term health just as seriously? The earlier you invest, the greater the return.

The Arketa portfolio includes "working less" as an explicit component. In practice, that might mean negotiating a four-day week - something increasingly possible, and worth asking for. Or choosing a self-employed route that gives you more control over your time.

Employers could go further: subsidised physical activity as a benefit, extended into retirement for long-serving employees. A far more imaginative use of a benefits budget than increased pension contributions.

💰 Financial capital - still matters, but not the only story

I'm not saying abandon your pension. Far from it. But treat it as one pillar among several, and think carefully about where it's invested.

When we think of values-aligned investing, we typically think about exclusions - e.g. avoiding fossil fuels. The deeper shift is moving your capital away from short-termism altogether, towards stewardship that considers the world your savings will retire into.

The Arketa portfolio points to two practical directions. A higher allocation to the Global South - less tied to the extractive growth model of developed markets - is something you can implement through many ethical fund platforms. For degrowth-aligned lending, in the UK, the Innovative Finance ISA typically funds exactly this kind of project: small-scale, community-beneficial, locally rooted. Forward-thinking employers could think to match IF ISA contributions as an alternative to additional pension matching - particularly as the tax benefits of pension contributions dilute as pots grow larger.

For most people on auto-enrolment pensions, making a "pension switch" to a personally managed SIPP is a bold move, but more achievable than you might think. For those with guaranteed benefits, a "pension transfer" requires regulated advice but is still possible. At a minimum, most providers offer a more ethical fund option. It's worth finding out what yours does.

👥 Social capital - who's in your bubble?

Before pensions existed, family and community networks were the retirement plan - and in many cultures, they still are. The people around you are not just a source of joy; they are a genuine form of resilience.

Who is in your social bubble when a future climate catastrophe hits? This isn't doom-mongering - it's a practical question that retirement planning increasingly needs to take seriously.

Many employers already facilitate CSR initiatives - volunteering days, community partnerships, charity matching. These are a start. But the multi-capital mindset invites something more ambitious: treating community engagement as a genuine employee benefit, not a box to tick. And crucially, extending that connection beyond retirement. Forward-thinking employers could actively support that transition - keeping retirees connected rather than letting the ties quietly dissolve.

🏡 Manufactured capital - your property and infrastructure

What's your property strategy? In the UK this is increasingly complex - not just because of affordability, but because flood risk, future "un-insurability", and energy costs are becoming real considerations in asset valuations.

There's a structural inefficiency worth naming. We contribute into financial markets for decades, hoping the returns will fund - amongst other things - energy bills in retirement. It's a long, uncertain chain. A more direct route is to reduce those bills at source: solar panels, heat pumps, better insulation. The earlier you act, the longer the payback period works in your favour.

Employers could play a role too - facilitating green home upgrade schemes, particularly in the years approaching retirement. The home as infrastructure, not just asset, is a framing worth taking seriously.

And then there's a more radical rethink: cohousing. Each household has a self-contained home but shares communal space and resources with neighbours. In the UK, Springhill in Stroud is one of the first purpose-built examples - timber-framed, solar-powered homes around shared gardens, a communal kitchen, and a rewilded space. This is where manufactured and social capital blur into one another. The community you live within is part of your infrastructure - and in a more uncertain future, that may matter more than the square footage of your house.

🧠 Human capital - working for longer, on your own terms

The idea isn't to resign yourself to working forever out of financial necessity. It's to stay engaged, contributing, and purposeful - because doing so is genuinely good for you.

People who maintain a sense of purpose and activity live longer and healthier lives. And in a world that urgently needs human effort directed at big problems, there's no shortage of meaningful work to do.

Ongoing investment in skills and education is central to this. The return - though harder to measure than a fund's annual performance - can often exceed financial returns. The ability to stay relevant, keep generating income, and pivot into work that matters is enormously valuable. It should be a no-brainer for employers to invest in their people's development throughout a career, not just in the years of peak productivity.

And it's a mindset worth adopting personally. In the same way you track your pension contributions, are you tracking what you invest in your own training and development each year?

🌱 Natural capital - your stake in the living world

We are all dependent on functioning ecosystems, whether or not our balance sheets reflect it. Taking active responsibility for nature - in your garden, your food choices, or through financial support of restoration - is not just good ethics. It's rational risk management.

Food provenance is a good place to start. Do you know how your food is produced - and whether it restores or depletes the soil it comes from? Employers could play an imaginative role here: sponsoring a regenerative farm that delivers sustainably grown food to employees and retired workers alike. Many employers already provide free fruit as a perk - this is just taking that idea a few steps further, and directing it somewhere that genuinely matters. Until that happens, you could start taking into your own hands with services like Riverford and Ethical Butcher amongst others, that deliver food direct from regenerative British farms.

Nature restoration projects - woodland creation, rewilding, peatland recovery - offer another practical way to contribute. Often positioned as carbon offsets, which carries controversy when used as a substitute for cutting emissions. But framed as straightforward philanthropy - supporting nature because it matters, not to balance a carbon ledger - that controversy falls away entirely. Ecologi is a great place to start exploring.

🗳️ Political capital - your legacy beyond inheritance

In the UK, pension assets are now subject to inheritance tax. The traditional idea of financial legacy is getting harder to execute. But your actions - your voice, your advocacy, your participation in civic life - carry forward in ways that compound in unpredictable and powerful ways.

Given the future your children face, it's worth asking whether they might actually value this kind of legacy more than a financial one. Have you asked them?

How are you contributing beyond just voting? This is part of what I'd call spiritual capital too - understanding your place in the world, and choosing to take responsibility for it.

🧭 Decisions capital - one the Arketa Institute didn't mention

The future world we're heading towards is a chaotic mess. Decisions will be increasingly difficult. Our life trajectory - and collectively, society's - is dependent on the quality of decisions being made.

Do you have a space or a framework for making quality decisions? If not, that is itself something worth seriously investing in.

The deeper shift: letting go of growth (or redefining it)

Underneath all of this sits a more fundamental reframe. Most of our current retirement system is built on the assumption of perpetual economic growth - that markets will be significantly higher in real terms in 2060 than they are today, and that this growth will be distributed widely enough to make pension funds viable.

That assumption is worth questioning. Not because economic activity will stop - but because the extractive model of growth that underpins much of the current system simply cannot continue indefinitely. Six planetary boundaries breached.³ Ecological debt accumulating. The direction of travel is not good. Deep down, I think we all know this.

There is a more hopeful version of this story: growth that is regenerative rather than extractive, powered by renewable energy, restoring rather than depleting natural systems. That future is genuinely possible. But here lies the real danger - the systemic risks we've been discussing could do serious, lasting damage before we complete that transition. The window matters. And a retirement system that bets everything on financial markets surviving intact through that window may be taking a risk its savers don't fully understand.

Moving towards a multi-capital mindset isn't just about protecting yourself. It's about "quiet-quitting a system" that isn't working - if you will - and, quietly, modelling something different for everyone around you.

Where to start

You don't have to overhaul everything at once. Here are four starting points:

- Check your pension fund. Find out what it's actually invested in. Most providers now offer an ethical or sustainable option and more people are making the switch than you might think.

- Audit your four health capitals. Physical, mental, social, spiritual. Where are you strong? Where have you been neglecting? Build a habit around the one that needs the most attention.

- Have a conversation. With a partner, a friend, a colleague. Not about ISAs or pension transfers - just ask: what does a good later life actually look like for you? You might be surprised where it leads.

- Get in touch. If any of this resonates and you'd like to explore what a multi-capital approach could look like for your own situation, I'd be happy to have a conversation.

The pension was invented as a bonus for outliving expectations. It has since become one of the most powerful forces shaping our global economy - and one of the most significant sources of both risk and potential in our collective response to the climate crisis.

We don't have to wait for the system to change. We can start with our own choices, our own habits, our own multi-capital plan. Every person who does is a proof of concept. Every conversation about it is a seed of something better. It inspires others. Then snowballs. That's eventually how systems transform.

With thanks to the authors of the Arketa Institute's post-growth pensions report, for inspiring much of the thinking in this article.

¹ The 1889 German Old-Age and Invalidity Insurance Law set the retirement age at 70. Male life expectancy at birth at the time was under 45 years. Source: Social Security Administration (ssa.gov/history) and Deutschlandmuseum.

² The 2021 Ahr Valley floods killed 190 people and caused approximately €33 billion in property damage — more deaths than all inland floods in Germany combined over the previous 40 years. Source: DKKV (German Committee for Disaster Risk Reduction).

³ Richardson et al. (2023), "Earth beyond six of nine planetary boundaries", Science Advances. Published by the Stockholm Resilience Centre, Stockholm University.

Disclaimer:

The information provided is for general informational purposes only and does not constitute investment, financial, tax, or legal advice. Please be aware that an investment strategy that is appropriate for one person, may not be appropriate to another, including yourself. Past performance is not indicative of future results. In tailoring your own personal investment strategy it is recommended to speak to a qualified professional.