The Art of Retiring Well

The hardest part of retirement isn't the size of your pension — it's the shape of your life. A reflection on the maths and psychology of retiring well.

I recently had the privilege of presenting twice at Retirement Matters, a conference held at the prestigious Royal College of Physicians. In my part-time actuarial role, I was there to help promote the launch of a new product - one designed to give retirees the confidence to stay invested in financial markets while still taking a regular income. As is typical for an actuary, my presentation was full of colourful charts and fancy maths.

And the maths of retirement is genuinely complex - something many at the conference acknowledged openly. There is still no one-size-fits-all solution. Most presenters offered their own take on that maths. But the presenter who stood out did something different: he argued that the psychology of retirement is every bit as complex - perhaps more so. The biggest source of wealth and happiness in later life, he noted, isn't money. It's your network.

For anyone planning their retirement - or guiding/advising someone who is - it's tempting to get drawn into optimising the numbers: investment returns, the cost of living, financial products, tax efficiency. But we shouldn't lose sight of the very human side - the hopes, dreams, fears and insecurities that come with one of the biggest transitions you'll ever face. Retirement is an art as well as a science.

This article is my attempt to give the art its due. But before we get to either the art or the science, it helps to be clear about what they are both in service of. Because a retirement is not a single cliff-edge, or a featureless stretch of time. It has a shape.

This article is another longer one. Retirement is a complex topic to talk about! - so grab yourself a cup of tea, or save this for a quiet moment on your commute.

Retirement has a shape

First, a confession: I use the word "retirement" reluctantly. These should be years of purpose and enjoyment, not redundancy - but it's still the word we all reach for, so I'll keep using it.

Picture your own retirement for a moment. Most of us imagine a fairly uniform stretch of time - and, as is well documented, most of us underestimate how long it will be. Perhaps it's easier to picture a loved one. I think of my Dad: at 82, still obsessed with playing golf at least three times a week, and still keeping up with us all gallivanting around Wales on family trips. Lately we've begun to broach the harder questions. What happens when golf is no longer possible? How will life change? And if his health deteriorates, how will my sister and I support him?

In those questions you can see the phases financial planners talk about: the go-go, slow-go and no-go years - an energetic, active start, a slower middle, a quieter and more dependent end. Or, more precisely: lifespan (how long you live), healthspan (how long you live well) and frailspan (the gap between them - the years lived in decline).

Each phase has its own needs and spending patterns, often concentrated early on. The real challenge isn't only how long we'll live, but how long we'll live well - and how we manage dependency at the end. That's not just a question of pension, but of family, network, and fallbacks like the family home.

Understanding this casts a new light on Memento Mori - Latin for "remember you'll die," a reminder to appreciate your life now. For retirement, perhaps Memento Senescere - remember you'll slow down - is the wiser idiom. Things possible early on may be out of reach later. I'm thankful we made our recent trip to Sri Lanka while we could, to reconnect with distant family - an opportunity that may or may not come again.

So a retirement has a shape, pieced together from parts: what your go-go years look like, what the no-go years will ask of you, how spending shifts in between. Understand those pieces, and you can begin to plan your wealth around them.

Life has to fit the shape

Once you see the shape, the temptation is to reach straight for the money - how big a pot, what income, which products. But there's an important principle at the heart of good financial planning: life before money. What is the end that the means needs to support.

When people leave work, many are surprised by how much the job was quietly providing beyond a salary. Psychologists who study retirement point to five things a working life supplies almost invisibly - five pillars that won't come with a simple pension cheque:

- Purpose - a reason to get up each day, a sense of contributing to something.

- Identity - an answer to "so, what do you do?".

- Relationships - a big proportion of our daily social contact arrives incidentally through colleagues, clients and the rhythm of work.

- Structure - the shape of a day, a week, a year, imposed whether we like it or not, and oddly missed once it's gone.

- Wellbeing - while work can often have negative connotations, for many the challenges of work keep our physical and mental health in check.

Credit to: Robert Atchley's The Sociology of Retirement, and Dan Haylett Humans vs. Retirement.

Notice, though, that none of these five sit still. Each has its own arc across the shape we just drew - and several behave remarkably like money: invested in the go-go years, drawn down in the slow-go and no-go ones. Planning a later life isn't about freezing a picture at the point you stop work. It's about designing each pillar to evolve - or to fade gracefully - across all three phases.

Two of them carry real leverage. Wellbeing is the one pillar that doesn't fit the shape - it bends it. The health habits you build in the go-go years are the single biggest lever on how long those years last, and how short the frailspan turns out to be. And relationships are the great long-term investment: the network you nurture while you're mobile and energetic becomes the support you lean on when you're not. Who's in your bubble when golf is no longer possible? - to borrow a question from my own family - is largely decided years earlier. It's exactly why that conference speaker put your network above your money.

The other three are about ageing well rather than fast. Identity holds steadier when it's anchored to who you are rather than what you do - because the doing falls away, first the job title, later the hobbies that replaced it. Purpose lasts when it's renewable and scalable, able to shrink from leading, to mentoring, to simply being present, without ever vanishing - perhaps a reinvested kind of work, on terms that finally suit you. And structure, designed lightly and early, becomes the scaffold you lean on more heavily as initiative fades.

All of which gives a sharper edge to a simple question: if money were no object, what would the first five years of your retirement actually look like? It isn't really a question about spending. It's about deciding what to invest in - health, people, purpose - while you still can. Get that right, and the money has something worth serving. So: how do you make the money fit a shape like this?

Money has to fit the shape

So we know the life we're funding. Now for the money - and here's where it gets genuinely hard, because pensions are getting riskier, not safer. For most of us, the sensible thing is still to stay invested through the go-go years, so the money keeps pace with inflation. It should be a gentler ride than the one that built the pot - a smaller rollercoaster, smoothed where it can be (the kind of approach I was at the conference to talk about). Even so, the core challenge remains: we're matching uncertain investment returns against an uncertain number of years left to live. And if you believe, as I do, that the wider economy rests on shakier foundations than we like to admit — a theme I explored in What if we invented the pension again from scratch? — then "markets always recover" becomes a riskier thing to lean on for thirty years.

Why the old rules don't quite fit the shape

Take the traditional "4% rule": start by drawing 4% of your pension pot in year one, and then increase with inflation each year. Twenty years ago that might have held. Today many argue investment returns will be too low, and inflation too high and "spiky", for it to be safe. But there's a deeper problem - a flat, inflation-linked income doesn't fit the shape at all. It hands you the same in your no-go years as your go-go ones, when what you actually want is more early and less late. Also the risk of suddenly running out in your final years, if you're in the unlikely cohort.

The "units, not pounds" idea - divide your pot by the years you expect to have left, and take that as an annual income - has the same flaw in reverse. If your investments beat inflation, you end up with less to begin and more later, climbing in a squiggly line as markets rise and fall. Again: the opposite of the shape.

Start with the floor

So the better instinct is (likely to be) to secure your basics first. The State Pension is a solid foundation. If you have a final salary scheme pension too, then you're in a highly enviable position for baseline security. But many do not. Instead, annuities are the classic way to turn a slice of your invested pension pot into a guaranteed income for life - peace of mind that markets can't touch.

Annuities do come with a catch, though: they're an all-or-nothing decision - once bought, you can't change your mind - which makes timing everything. In 2022, someone who annuitised at the end of the year secured roughly 50% more income than at the start, as rates hit a fourteen-year high. On value-for-money grounds, many argue for waiting until around 80, when the maths tilts in your favour - though by then, who knows what your pot will be worth. One sensible middle path is to buy in bite-size pieces over time, rather than stake everything on a single day's quote.

Earn a little, hedge a lot

Then there's the most underrated move of all: keeping some paid activity on your own terms. It eases the pressure on every one of these difficult financial decisions - and it's a natural hedge. In your go-go years you're both more able to work and more inclined to spend; a little enjoyable, paid activity can fund life's extras exactly when you most want them. Not working because you have to. Working because it pays for the good stuff - and keeps the pillars standing too.

And then - actually spend it

Which brings us to the hardest part of all, and it isn't a number. It's the trap of reaching the end with too much left, simply because you were too afraid to spend. That fear is real and widespread - three in five UK adults worry about having enough income in retirement - yet the IFS finds the bigger problem is the reverse: most pensioners draw down so cautiously that they leave substantial wealth unspent at the end of their lives. The tragedy is that the fear is paid in the one currency you can't get back: your go-go years.

So how do you avoid it? Write the bucket list - the last one you'll ever make - and prioritise it honestly: what you must do, what you'd like to, what you could let go. Secure your basics beneath it. Then it's a matter of planning the messy middle in between. Earning and investing-to-reduce-expenses both make that middle far easier to manage - on the property side, that can mean retrofitting the home you already own (solar, battery, insulation etc.) so a slice of capital becomes bills you never pay again, or downsizing to free some up. And finally, build in flex: a strategy loose enough to bend with whatever the next thirty years throw at it.

Because the goal was never the biggest possible pot. It was a life worth the saving.

The Art is Harmony

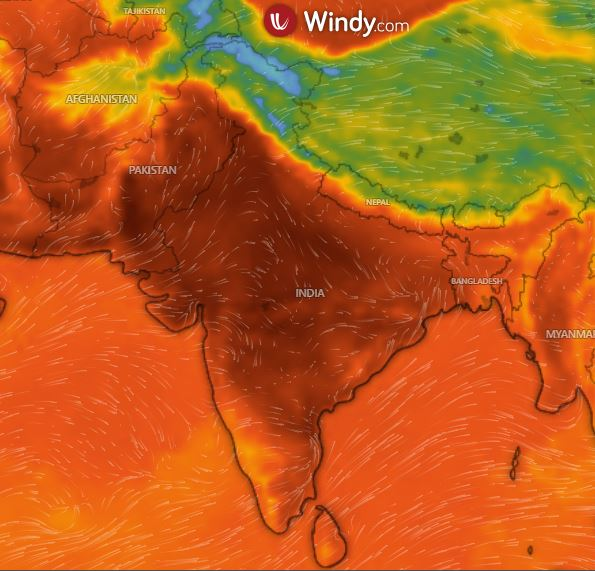

I'm writing this article in the middle of the mammoth May heatwave in the UK, and most of the talk I see online is - understandably - about how as a nation we plan to cope with this going forward. But honestly, the scariest thing I've looked at this week isn't the UK weather forecast. It's the map below of India, currently enduring something far worse. Many large cities enduring 45+C temperatures. Getting scaringly close to the 'wet bulb' temperature, when any human life struggles to survive.

What does this picture look like in the next 10, 15, 20 years? What will the repercussions be for the world's most populous country, as well as similar impacts happening elsewhere? Will the financial markets (in which our pensions are invested) ride these repercussions without flinching? Will the cost-of-living and inflation politely stay in its lane? Ultimately, nobody really knows.

A future like we've never seen, but where ancient Roman wisdom feels just as relevant. Memento mori - remember you'll die. Memento senescere - remember you'll slow down. Collectively we need to appreciate the moment. In a dualistic sense: An honest acceptance that much of the world and our bodies will never be the same. Whilst at the same time a stubborn insistence on living the years you've got, and on leaving something better behind. Neither denial nor despair. A fine (harmonious) balance in between.

But to end on a hopeful note. The dial is shifting slowly - the IPCC did recently take away their most extreme climate scenario for the future, due to human ambition on implementing renewables. Human action can start to shift the dial in the right direction. But nonetheless, the range of outcomes of what remains still looks perilous, and climate change is only 1 of 7 planetary boundaries in highly dangerous territory.

Hopeful from a personal perspective. The things worth holding on to most are also the ones potentially least exposed. A healthspan you've invested in. A network you've nurtured. A purpose that pays a little and means a lot. A guaranteed floor for your essentials. A home that costs less to run. None of that hinges on which way markets break, or what the next decade does to the wider world. It hinges on you.

And, quietly, each of those choices is also a kind of refusal - of the idea that a good retirement means accumulating more and consuming harder. Purpose that helps, not just pays. A retrofit that lowers your bills and your carbon. Experiences chosen over things. The most lasting legacy, it turns out, rarely lives in a will. It lives in what you stood for, the people you led, the words you said out loud. The shape of how you spent the years. The trip to Sri Lanka while you still could. The work that mattered. The home that gave back. It's the gentlest answer I know to a future we can't predict: live a life that holds up, whichever way the world goes.

Which is exactly why it's worth starting now - not in anxiety, but in conversation. With a partner, a friend, and a coach or guide you trust. About the life you actually want to live, and the shape of the years you've got to look forward to.

If this piece resonated, please do subscribe. And if it sparked reflections or questions of your own, I'd genuinely like to hear them — hit reply, or drop me a line at neil@planetpositiveplanning.com.

Disclaimer:

The information provided is for general informational purposes only and does not constitute investment, financial, tax, or legal advice. Please be aware that an investment strategy that is appropriate for one person, may not be appropriate to another, including yourself. Past performance is not indicative of future results. In tailoring your own personal investment strategy it is recommended to speak to a qualified professional.